RESEARCH MEMORANDUM

Venezuelan Monetary Recirculation:

Mechanism, Inventory, and Convergence

Dublin, Ireland | Montréal, Québec

Not for dissemination without the author's written consent | All rights reserved © 2026 MIGP Capital Corporation Inc.

THE PROPOSITION

In vaults belonging to the Banco Central de Venezuela sit roughly three-quarters of a billion banknotes that have never touched a human hand. They were produced by the world's leading security printers, paid for in full — about $53 million — and never issued. Venezuela's monetary collapse simply moved faster than its printing contracts.

This memorandum argues that those notes are about to come back.

The argument rests on a fact almost nobody notices: Venezuela has never actually replaced its money. Twice it struck zeros from the currency — five in 2018, six in 2021 — but the unit was the Bolívar before and it is the Bolívar now, and the notes themselves say only bolívares. No series name, no conversion factor, appears on any of them. A note printed in 2017 reading 10,000 Bolívars is, physically and linguistically, a 10,000-Bolívar note today — worth about $14 at the current exchange rate. Whether it counts as money is not a question of printing. It is a question of one resolution by the central bank's Board.

Meanwhile, the country is running out of cash in a way that is difficult to overstate. The highest-denomination banknote in Venezuela is today worth less than one US dollar, and it loses value daily. The nation's entire stock of physical cash works out to roughly five dollars per person; the comparable figure for Canada is about $2,200. The central bank is distributing new notes as fast as it can — this research documents it from the central bank's own files — but every note it can currently print is worth under a dollar. The only inventory of usable denominations within reach is the one already sitting in its vaults.

And for the first time since sanctions closed over the country in 2017, everything else lines up. Maduro is gone. The sanctions on the central bank are lifted. The IMF office is in the BCV building. The man who designed the 2018 monetary framework has just been named president of the country's largest retail bank. The exchange rate has entered — and is now consuming — the precise band in which redeploying the old notes makes arithmetic sense.

This thesis names its own deadline: on the current trajectory, that window closes on or about 21 July 2026. Either something happens, or this memorandum is wrong in a way it has promised, in writing, to admit.

What follows is the evidence. The summary gives the shape of it in one page; the sections give the vaults, the law, the border markets, the price data — and the ways to prove it false.

SUMMARY

The claim. The Banco Central de Venezuela is positioned to recirculate its legacy banknote inventory — declaring high-denomination notes printed in 2016–2018 legal for circulation at their face value in Bolívars — as the fastest, cheapest, and only timely way to rebuild the country's collapsed cash layer. The thesis holds that this occurs while the exchange rate remains inside the 600–800 Bolívars-per-dollar window, which at the current pace of depreciation closes on or about 21 July 2026.

The law already permits it. Venezuela's currency reforms rescaled the Bolívar; they never replaced it. The notes carry no series identifier and no conversion factor, UK customs and the international currency-code registry already treat the old and new codes as the same instrument at one-to-one, and part of the legacy inventory was never stripped of its legal circulating status at all. What remains can be restored by a single resolution of the central bank's Board — no legislation, no lead time. The memorandum states the one legal subtlety honestly: notes that were formally demonetised require an affirmative act of re-monetisation, which is available under the Bank's issuance powers but without international precedent.

The notes exist and are paid for. Approximately 750 million unissued notes sit in vault storage — roughly $53 million in sunk production cost, against an 18-month minimum lead time for any newly designed replacement family. The central bank's own circulation files, thirty-five snapshots of which are archived by this research, show it has never written any of the legacy stock off: balances are frozen on its books, carried unchanged for years, and then quietly removed from view — never cancelled. By the Bank's own accounting, 63% of the old high-denomination family was never handed back, meaning a recirculation at face value would also deliver a windfall to whoever still holds those notes — a deliberate, near-costless recapitalisation of household balance sheets. The injection is large — the vault stock alone is 27 times the country's entire current physical cash — but it is meterable, partitionable, and directed at an economy holding five dollars of cash per person.

Someone was already buying the notes back. For years, a border money market in Colombia absorbed a one-way flood of Venezuelan cash that no natural demand could explain — and cleared it, daily, without inventory ever accumulating. The flow included factory-sealed sequential bricks that can only originate in institutional packaging. The market died within weeks of inferior new notes entering circulation — exactly what the withdrawal of a quality-sensitive institutional buyer would produce. The most coherent identity of that buyer is the central bank itself, quietly recovering its own best paper.

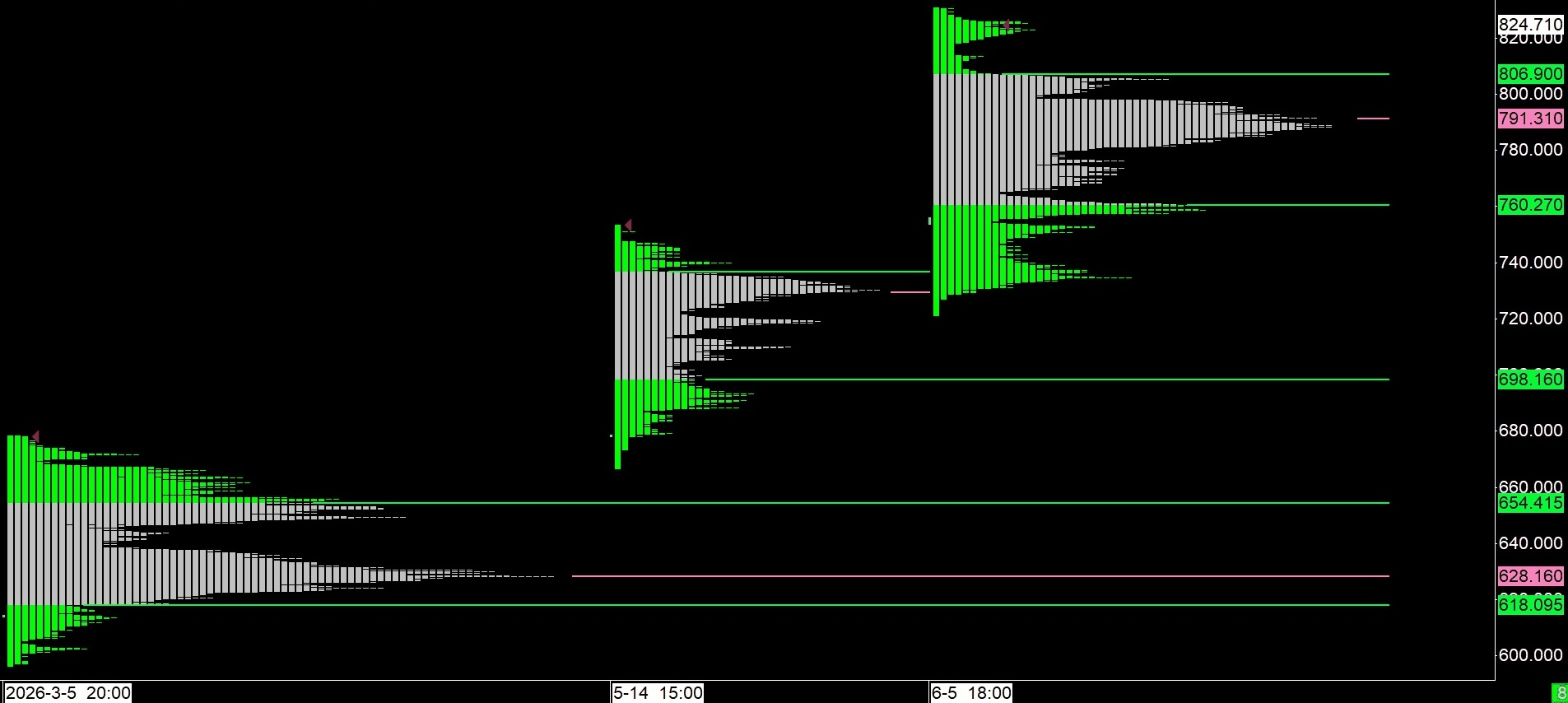

The price data agrees. A single structural devaluation line has governed the Bolívar for fourteen years — the currency's dollar price doubling roughly every seven months — touched by the market seven times across two reconversions. The one period the line was ignored is the one period the central bank openly administered the rate: the line yields only to management, and management is precisely what a recirculation restores. Today the rate sits far above that line, and the parallel market has formed a confirmed fair-value zone at 760–807. Two independent calculations — one from the official rate's velocity, one from the parallel market's structure — converge on the same coordinates: the two rates meet inside that fair-value zone around 20 July.

The projection. An announcement inside the window; a brief period of weakness as windfall holders sell; stabilisation — for which the central bank ran the exact template in 2023–24; then a reserve-backed appreciation toward 100–300 Bolívars per dollar around the January 2027 inauguration. That target is not a return to trend — it is a deliberate break of the fourteen-year devaluation regime, attempted for the first time with gold, IMF access, sanctions relief, and a debt restructuring behind it.

What would prove it wrong. A tender for a newly designed note family; formal cancellation of the remaining legacy notes; physical disposal of the vault stock; or the exchange rate exiting 800 with no announcement and no visible defence. These criteria are stated in advance, in Section 5.8, and the memorandum accepts being judged by them.

Sections I through V then supply, in order: the legal architecture, the physical inventory, the market evidence, the price-structure analysis, and the convergence projection.

SECTION I: LEGAL AND INSTITUTIONAL ARCHITECTURE

Venezuelan monetary history since 2008 is not a sequence of distinct currency replacements. It is a single continuous legal instrument — the bolívar — repeatedly relabelled, rescaled, and re-expressed by the same issuing authority under the same constitutional framework. Every reconversion event examined in this section left open a legal door that the BCV declined to close. Those open doors, accumulated across eighteen years of monetary architecture, now constitute the legal basis for redeploying existing physical note inventory without a new printing programme.

1.1 The Bolívar Fuerte — Foundation of the Physical Inventory

The Bolívar Fuerte (Bs.F) entered into force on 1 January 2008, replacing the old bolívar at 1,000:1 — three zeros removed. The BCV simultaneously deposited gold reserves at the Bank of England, opening Account 217 "Banco Central de Venezuela" and Account 571 "Banco Central de Venezuela Number 2" (opened 12 August 2008 — the same year the Fuerte launched). These accounts remain the subject of ongoing litigation directly relevant to the recirculation scenario (see Section 1.9).

The Fuerte family as originally issued comprised denominations of 2, 5, 10, 20, 50, and 100 bolívares. By 2015 inflationary pressure had rendered even the highest denominations inadequate for daily commerce, and the BCV was under significant operational pressure.

In late 2015, the BCV placed a major forward order covering both the Bolívar Fuerte high denomination series and the Bolívar Soberano 2018 UK-printed series — a combined forward order representing the BCV's entire planned monetary transition architecture. The full detail of this tender, including source documentation and arithmetic, is analysed in Section 2.2.

The 2016–2017 Fuerte high denomination ampliación was formally announced on 4 December 2016. A BCV press note of 16 January 2017 confirmed the series. On 22 February 2017, the first shipment arrived from G+D in Sweden — 30 million pieces of the 1,000 Bs.F note in 600 boxes. The notes carry the full suite of premium security features: windowed security thread with demetallised BCV text, Simon Rodríguez watermark, electrotype denomination watermark, and full intaglio printing. No note in the series identifies itself as a "Bolívar Fuerte." Every note reads simply "BOLÍVARES" — the same word used across every subsequent monetary series. Physical dimensions: 156 × 69 mm across all series.

1.2 The Payment Crisis and Its Cause

The Infosecura article confirmed that De La Rue began experiencing payment delays as early as June 2015. The BCV was similarly slow to pay G+D and Oberthur Fiduciaire. When the 10.2 billion note tender was offered, the government received only about 3.3 billion in bids because the printing companies were concerned about payment.

The cause of these payment delays is definitively established by a primary source of the highest available quality: the De La Rue plc Annual Report and Accounts 2019, filed with the UK Financial Conduct Authority on 21 June 2019, audited by Ernst & Young LLP.

The report states in multiple places:

"£18.1m credit loss associated with the outstanding accounts receivable of a customer in Venezuela currently unable to transfer funds due to non-UK related sanctions."

The auditors' Key Audit Matter section states:

"As a result of the US sanctions upon Venezuela, Banco Central de Venezuela have been unable to settle their open receivables to De La Rue."

These are not editorial assertions — they are statements in audited financial accounts confirmed by a Big Four auditor. De La Rue examined "the nature & timing of US sanctions, our knowledge of positions adopted by other companies and the ability to receive settlement through alternative means" and concluded that the BCV was unable to pay specifically because of US sanctions blocking payment mechanisms, not because of insolvency or unwillingness.

A note on reconciling the figures: Infosecura (2016) reported De La Rue's outstanding Venezuelan receivable at approximately $71 million as of mid-2016, while the 2019 accounts recognise an £18.1 million credit loss. The figures are measured at different dates, in different currencies, and on different bases — a gross trade receivable versus a recognised accounting impairment after recovery assessment — and are complementary data points rather than a discrepancy.

There were no UK sanctions on Venezuela at the time. The BCV had the obligation and the intention to pay. The US government's interference with SWIFT transactions blocked the payment. The Goznak emergency engagement that followed was therefore a forced consequence of US sanctions policy — not a reflection of the BCV's preferences or institutional competence on the specific question of printer payments. The recirculation thesis's preference for G+D, De La Rue, and Oberthur Fiduciaire — all Western companies now explicitly within the authorised framework — is therefore consistent with the current US sanctions architecture. The OFAC framework's exclusion of Russian-linked entities, and its implications for any future Goznak engagement, are addressed in Section 2.1 (Tier 4a).

A precise distinction is required: the De La Rue evidence establishes that the BCV had the intention to pay and that the mechanism was blocked externally. It does not establish broader BCV institutional good faith across all monetary management. The underlying fiscal crisis — exponential money supply growth from fiscal deficits financed by BCV credit to the government — was domestically generated and preceded the major financial sanctions of August 2017. External sanctions blocked a specific payment channel; domestic monetary policy created the crisis that made the resulting supply chain disruption catastrophic. This research's argument rests on the former; it does not rely on the latter.

With OFAC General License 57 in effect from 14 April 2026, the direct sanctions barrier to settlement that De La Rue's auditors documented has been substantially removed — though Venezuelan hard currency revenues now flow through a US Treasury-supervised account structure (see Section 5.1), meaning the full picture of BCV's payment freedom requires nuance.

1.3 The Reconversion Machinery — Decrees 3.332 and 3.445

Decree 3.332 (22 March 2018): Published in Gaceta Oficial N° 41.366, this decree planned the monetary reconversion at 1,000:1 — three zeros removed. The original plan was not five zeros. The new unit was to be equivalent to one thousand existing bolívares, scheduled for 4 June 2018.

This matters: at a 1,000:1 ratio, the 100,000 Bs.F note would have mapped to 100 — identical to the 100 Bs.S note later created. Co-circulation under that mapping would have been visually intuitive. The five-zero conversion ultimately adopted destroyed that visual continuity and made co-circulation more psychologically disruptive. The original plan was decreed under the State of Economic Emergency framework — establishing that monetary reconversion is an executive act requiring no ordinary legislative procedure.

Decree 3.445 (1 June 2018): Published in Gaceta Oficial N° 6.379 Extraordinario, this deferred the reconversion and carries two provisions of direct legal relevance.

First, the countersignature of Tareck El Aissami as Executive Vice President — an individual designated under the U.S. Kingpin Act on 14 February 2017, seventeen months before signing this monetary instrument.

Second, and most critically, Article 2:

"El Banco Central de Venezuela determinará mediante Resolución de su Directorio [BCV Board of Directors] las denominaciones de los billetes y monedas metálicas por él emitidos, representativos de la unidad monetaria actual, que podrán circular con posterioridad al 4 de agosto de 2018, conservando su poder liberatorio hasta que sean desmonetizados conforme a lo que indique dicho Instituto Emisor."

This establishes three things simultaneously: the BCV Board of Directors has sole authority to determine which denominations continue to circulate; those notes conserve their poder liberatorio by active BCV determination, not by automatic legal consequence; and demonetisation occurs only "as and when the BCV itself indicates." There is no automatic expiry, no external authority, no date certain.

1.4 The August 2018 Package — Ortega, the Soberano, and Free Convertibility

On 19 June 2018, Decree 3.474 appointed Calixto José Ortega Sánchez (cédula V-16.834.560) as BCV President under emergency powers, countersigned by Delcy Rodríguez. The National Assembly challenged the appointment; the TSJ declared their challenge unconstitutional. Ortega remained in post. He served as BCV President from June 2018 until February 2023, when he was succeeded by Miguel Ángel Pérez Abad. Pérez Abad served from February 2023 to April 2025, presiding over the monetary stabilisation period documented in Section IV.

He was followed by Laura Carolina Guerra Angulo (April 2025 to April 2026), who resigned days after OFAC General License 57 lifted BCV sanctions. Acting President Rodríguez immediately appointed Luis Pérez as BCV President — the same institutional authority who countersigned Ortega's original 2018 appointment now placing a new BCV head in post to operate in the first unsanctioned environment since 2019.

By the time of the 30 May 2026 IMF meeting, Ortega attended as Economy Vice President alongside BCV President Luis Pérez.

On 20 August 2018, the Bolívar Soberano entered into force at 100,000:1 from the Fuerte. ISO 4217 Amendment 168, effective the same day, introduced VES/928 — but with one critical sentence: "The expiration date of the aforementioned circulation will be defined later and communicated by the Central Bank in due time." The international monetary authority acknowledged from day one that the BCV retained sole discretion over the demonetisation timeline of legacy Fuerte notes.

On 21 August 2018 — the day after the Soberano launched — BCV Board of Directors Session N° 5.105 authorised Ortega to sign Convenio Cambiario N° 1, published in Gaceta Oficial N° 6.405 Extraordinario. Countersigned by Finance Minister Simón Alejandro Zerpa Delgado, this instrument abolished exchange controls and restored free convertibility — the most significant exchange rate liberalisation in decades, executed on the first full business day of the new currency's existence.

The Bolívar Fuerte family was formally demonetised on 3 December 2018 by BCV Resolution 18-11-01, published in Gaceta Oficial N° 41.536. This was a clean, unambiguous, denomination-complete demonetisation — the contrast with the 2024 resolution is analysed in Section 1.6.

1.5 The 2021 Nueva Expresión Monetaria — The Nominal Continuity Doctrine

On 1 October 2021, Venezuela introduced the "Nueva Expresión Monetaria" — removing six zeros at 1,000,000:1. The resulting unit remained simply "bolívares" in the operative legal text. BCV Resolution 21-08-01 explicitly confirmed that Soberano-era notes including the Bs.S 50,000, 200,000, 500,000, and 1,000,000 would retain legal tender status "until the BCV decides otherwise." BCV Resolution 22-04-01 of 21 April 2022 subsequently governed the cessation of the double expression co-circulation period.

ISO 4217 Amendment 170, issued in October 2021, introduced VED/926 explicitly "for any internal needs during the redenomination process" — and stated directly that VED/926 was "not replacing VES/928 as the official currency code." In 2018, when a genuinely new currency was created, the ISO created a new code. In 2021, it declined to do so. That asymmetry is the ISO's own determination that the 2021 event was not a monetary replacement — it was a numerical rescaling of the same instrument.

This is the nominal continuity doctrine: Venezuela can rescale its currency — remove zeros, redefine the unit of account — without creating a new currency identity. The name persists. The issuing authority persists. The ISO code persists. Only the numbers change. This is the legal foundation on which a future recirculation of Fuerte-era notes under a new legal tender declaration at face value in Bolívars would rest.

1.6 BCV Resolution 24-08-01 — The Incomplete Demonetisation of 2024

BCV Resolution N° 24-08-01, published 29 August 2024, requires careful legal reading. Its precision reveals a deliberate choice not to close the monetary chapter it ostensibly addresses.

Article 1 names four specific denominations losing poder liberatorio (the implied legal freedom to circulate as a means of settling obligations — distinct from an express legal tender declaration, and extinguished only when the BCV explicitly revokes it) on 25 September 2024: the Bs.S 10,000, 20,000, and 50,000 notes — the Goznak Tier 4a series — and the Bs.S 200,000 note from the printer-unidentified Tier 4b series. The language is unambiguous: "perderán su poder liberatorio."

Article 2 addresses notes and coins "equal to and below" Bs.S 200,000, stating they may be deposited at banking institutions until 30 September 2024. This is a deposit deadline — a procedural, logistical provision. It does not contain the phrase "perderán su poder liberatorio." It does not strip any note of its poder liberatorio.

The Bs.S 2, 5, 10, 20, 50, 100, 200, and 500 notes — the entire premium-quality 2018 UK-printed Soberano series — and all coins are swept into Article 2's deposit window but retain their poder liberatorio. No subsequent resolution is known to have revoked it.

The BCV demonstrated with the December 2018 Fuerte demonetisation that it executes blanket demonetisations cleanly and completely when it chooses to. Two readings of the 2024 resolution's incompleteness are nonetheless available, and intellectual honesty requires weighing both. The mundane reading is that non-demonetisation is simply the BCV's low-cost default: formally demonetising denominations whose aggregate value had become economically negligible was not worth a decree — the same logic by which the 1,000,000 Bs.S was later allowed to decirculate naturally without one (Section 4.2). This research does not dispute that institutional inaction is cheap.

What the mundane reading cannot explain is the drafting asymmetry within Resolution 24-08-01 itself: Article 1 names four denominations and applies the operative phrase "perderán su poder liberatorio" with precision, while Article 2 sweeps the remaining eight denominations and all coins into a deposit-deadline clause that conspicuously omits the operative phrase. A drafter defaulting to inaction does not draft at all; a drafter who distinguishes, within a single instrument, between notes that lose their poder liberatorio and notes that merely face a deposit deadline has made a deliberate distinction. It is that asymmetry — not the bare fact of non-demonetisation — on which the optionality inference rests.

A necessary legal distinction — continuation versus re-monetisation. The two recirculation tiers stand on different legal footings, and the distinction should be stated plainly rather than left implicit. The Tier 3 Soberano denominations retain their poder liberatorio: their deployment requires no legal act beyond distribution and, at most, a confirming Board resolution. The Tier 2 Fuerte denominations do not — Resolution 18-11-01 demonetised the Fuerte family completely in December 2018. Their redeployment is therefore not a continuation but an affirmative act of re-monetisation, and Article 2 of Decree 3.445 — which governs the deferral of demonetisation for notes still conserving their poder liberatorio — is arguably exhausted with respect to notes already demonetised under it. The affirmative legal basis for Tier 2 lies elsewhere: in the exclusive faculty to issue especies monetarias conferred on the BCV by its organic law and exercised by Board resolution, which includes the power to determine the denominations and characteristics of the notes representative of the monetary unit.

Two consequences follow. First, the never-issued vault stock occupies a legally cleaner position than publicly held notes: a note that never entered circulation can be put into circulation by a fresh issuance resolution declaring the existing physical instrument representative of the current monetary unit at its face value in Bolívars — an act of issuance, not the reversal of a demonetisation.

Second, the publicly held Fuerte notes are the harder case, requiring re-monetisation proper — an act for which no clear international precedent exists. The BCV could lawfully recirculate the vault stock without re-monetising publicly held notes, which would cap the monetary injection quantified in Section 2.9 but forfeit the wealth-distribution effect described in Section 3.3.

Whether the Board would treat the two note populations identically or separately is a design variable of the recirculation, not a defect of the thesis — but the legal argument for Tier 2 must rest on the issuance faculty, not on Article 2 alone.

1.7 The ISO 4217 Framework and the Sierra Leone Precedent

| Amendment | Date | Event | Key Provision |

|---|---|---|---|

| 168 | 20 Aug 2018 | VEF → VES (100,000:1) | Introduced VES/928. Expiration of VEF "to be defined later by the BCV." Discretion explicitly acknowledged. |

| 170 | Oct 2021 | Nueva Expresión Monetaria | VED/926 "for internal needs only." Explicitly NOT replacing VES/928. ISO treats 2021 as non-event. |

| 171 | Apr 2022 | Sierra Leone SLL → SLE | Same nominal continuity language. Old and new notes co-circulated. Visually near-identical notes — only the numeral changed. |

| 175 | Mar 2023 | Sierra Leone extension | Co-circulation extended to 31 Dec 2023 — new notes took longer to print. ISO accommodates indefinite co-circulation. |

The Sierra Leone case (Amendments 171 and 175) is the closest real-world parallel in the ISO amendment record. Sierra Leone removed three zeros from the leone effective 1 April 2022. The old 2,000 leone note and the new 2 leone note are visually near-identical: same portrait of I.T.A. Wallace-Johnson, same building on the reverse, same colour scheme. Only the numeral changed. Sierra Leone needed new notes and still required a two-year co-circulation extension. Venezuela already has the notes.

The asymmetry between Amendment 168 (2018) and Amendment 170 (2021) is the ISO's own confirmation of the nominal continuity doctrine developed in Section 1.5.

1.8 The HMRC Notice — UK Administrative Confirmation

On 26 January 2026, HMRC published a Trade Tariff notice updating the Venezuelan currency code from VED to VES, effective 1 February 2026. The notice describes VES as "the official currency of Venezuela." No conversion factor is provided — the implicit exchange rate between VED and VES in UK customs declarations is 1:1.

This administrative determination confirms that VES — not VED — is the operative currency identity in UK trade law. The Bolívar Digital of 2021 never fully supplanted VES internationally, consistent with the ISO's own refusal to retire VES/928 in Amendment 170. The 1:1 implicit treatment means HMRC does not recognise the 1,000,000:1 rescaling of October 2021 as a monetary event requiring conversion — exactly the analytical position taken by the author of this research in maintaining an unadjusted continuous trading dataset.

1.9 The Bank of England Gold — Litigation and Recovery

Venezuelan gold held at the Bank of England in Accounts 217 and 571 became subject to litigation beginning in 2020. Public reporting has cited holdings of approximately 14 tonnes as of 2018, with subsequent accounts citing figures of up to 31 tonnes.

At current gold prices the holdings represent a substantial reserve asset — the precise quantum and current dollar value remain subject to the litigation record and gold price movements at the time of any recovery. The UK Supreme Court (December 2021) confirmed HMG's recognition of Guaidó was "clear and unequivocal" under the "one voice" doctrine. The High Court remitted hearing (July 2022) ruled British courts were not required to recognise Venezuelan TSJ judgments favouring the Maduro board.

The legal basis for blocking gold access has been substantially undermined by Maduro's capture and Rodríguez's emergence as acting president. The OFAC removal of Rodríguez from the SDN list on 1 April 2026 opens the political recognition pathway. Rodríguez has publicly named the BoE gold as a target recovery asset.

A specific technical advantage of the BoE gold is worth noting: Chávez's 2011 repatriation order caused the domestically held Venezuelan gold to lose its "Good Delivery" certification — the standard classification required for acceptance in international markets.

The gold remaining in the Bank of England accounts in Accounts 217 and 571 did not undergo repatriation and therefore retains its Good Delivery status, making it significantly more liquid and internationally tradeable than the domestic holdings. The BoE gold is therefore not merely a larger reserve asset — it is a qualitatively superior one.

Note: Even if the UK courts clear the gold for BCV access, the broader pattern of US oversight of Venezuelan assets — including oil revenue controlled through US Treasury deposit funds under Executive Order 14373 — creates uncertainty about whether repatriated gold proceeds would also be subject to US supervision.

Whether recovered BoE gold would enter BCV-controlled reserves or a US-supervised account is a scenario variable that materially affects the appreciation pathway. This remains an unresolved question in the current political arrangement.

1.10 The Sanctions Normalisation Sequence

| Date | Event | Significance |

|---|---|---|

| 3 Jan 2026 | Maduro captured | Removes primary obstacle to normalisation. TSJ creates hybrid ruling avoiding formal absence declaration. |

| 26 Jan 2026 | HMRC VED→VES notice | First UK administrative act normalising the post-Maduro state. Implicit 1:1 confirms nominal continuity. |

| 1 Apr 2026 | OFAC removes Rodríguez from SDN | Acting President no longer designated. Political recognition pathway opens. |

| 14 Apr 2026 | OFAC General License 57 | Authorises financial services transactions involving the BCV — wire transfers, currency exchange, and correspondent banking. Self-executing only when all conditions are met; must be read narrowly. Does not constitute a blanket lifting of sanctions. |

| 30 May 2026 | IMF MD Georgieva meets Ortega | First in-person IMF-Venezuela meeting since formal engagement resumed. |

| 5 Jun 2026 | IMF appoints Venezuela mission chief | Álvaro Piris Chavarri appointed. Article IV consultation underway. $150 billion restructuring referenced. |

| 18 Jun 2026 | OFAC General License 24A | Supersedes GL 24 (2019). Authorises telecommunications and mail/package transmission involving the Venezuelan government — restoring ordinary communications infrastructure access after seven years. |

| 18 Jun 2026 | OFAC General License 59 | Authorises US-person maintenance, repair, and airworthiness services for Conviasa aircraft. Explicitly excludes gold-denominated and petro cryptocurrency payment, and excludes Russian, Iranian, North Korean, Cuban, and Chinese-linked entities — confirming the Western-printer-only framework applied throughout this thesis. |

| 18 Jun 2026 | OFAC General License 5X | Supersedes GL 5W. Authorises transactions in the PDVSA 2020 8.5% Bond, effective 4 August 2026 — a forward-dated normalisation milestone. |

| 19 Jun 2026 | Rodríguez–Figuera talks | Jorge Rodríguez (National Assembly President) meets Dinorah Figuera, former opposition lawmaker returning after seven years in Spain — first public government–opposition rapprochement in nearly three years, focused on CNE strengthening. US State Department publicly welcomed the talks. |

| 29 Jun 2026 | Anabel Pereira Fernández appointed Vicepresidenta Sectorial Administrativa y de Gobierno Digital | Economist and lawyer, simultaneously retaining her roles as Ministra del Poder Popular para la Economía, Finanzas y Comercio Exterior and President-in-Charge of the Fundación Patria (appointed January 2026). Three simultaneous roles — Economy Ministry, Fundación Patria, and Digital Government — place a single technically-trained economist at the intersection of the three institutional functions a Bolívar recirculation would require to execute at scale. |

| Jul 2026 | Venezuela 2026 Petroleum Framework published in Official Gazette | First comprehensive petroleum regulatory framework since 1943. 29-page document formally authorises private sector participation across the full petroleum value chain with no direct reference to PDVSA. Key elements: 30% standard royalty (reducible to 15% for marginal and ultra-heavy fields), independent international arbitration, and direct crude marketing rights for private JV partners. Implementing regulations accelerated in July 2026. |

| 9 Jul 2026 | Rodríguez formal letter to King Charles III requesting BoE gold release | Acting President formally requests release of approximately 31 metric tonnes of Venezuelan gold held at the Bank of England, valued at approximately $4.2 billion at prevailing July 2026 gold prices per contemporary reporting, invoking earthquake reconstruction needs. Converts the ongoing BoE litigation (Section 1.8) into an active head-of-state diplomatic request alongside the parallel legal proceedings. |

| 9 Jul 2026 | Calixto Ortega Sánchez appointed President of Banco de Venezuela | While retaining his role as Economy Vice President (Vicepresidencia Sectorial de Economía). Ortega served as BCV President June 2018–February 2023 and is the architect of the entire 2018 monetary framework on which this thesis is built. He now simultaneously controls macro-economic policy coordination (Economy VP) and Venezuela's largest commercial retail banking distribution network (Banco de Venezuela) — the precise two institutional levers a Bolívar recirculation would require to be executed and distributed at scale. |

By July 2026, the institutional conditions have converged more completely than at any prior point. The OFAC sanctions architecture has been systematically normalised across six general licenses in three months. The 2026 Petroleum Framework represents the most comprehensive regulatory opening of the Venezuelan energy sector since 1943.

The BoE gold litigation has been elevated to a head-of-state diplomatic request. The IMF engagement has progressed to discussions of Venezuela accessing its own reserve tranche. And Calixto Ortega — the architect of the 2018 monetary framework — now simultaneously holds the Economy Vice Presidency and the Presidency of Banco de Venezuela, while Anabel Pereira Fernández holds the Economy Ministry, Fundación Patria, and Digital Government.

Between them, this team controls every institutional lever the recirculation mechanism would require to execute. The question is no longer whether the legal mechanism exists or whether the institutional conditions are present. Both are confirmed. The question is timing.

SECTION II: PHYSICAL INVENTORY — THE VAULT STOCK

The legal architecture documented in Section I established that the BCV possesses the discretionary authority to restore legal tender status to existing physical note inventory. This section establishes what that inventory is, how it was quantified using the BCV's own published data, and why a sufficient quantity has remained in institutional custody since the notes were printed. The physical inventory is not a theoretical construct — it is a documented, quantified asset with a known production cost, a known quality profile, and a known denomination structure from which a reconversion can be built without printing a single new note.

2.1 The Six-Tier Note Architecture

Venezuela's physical monetary inventory since 2008 was produced across six distinct tiers, each representing a different printing arrangement, quality level, security feature depth, and recirculation suitability. Understanding the tier structure is essential to evaluating which notes are candidates for recirculation and which are not.

Tier 1 — Bolívar Fuerte (VEF / Bs.F) | G+D / De La Rue / Oberthur | Original Family | 2 · 5 · 10 · 20 · 50 · 100

The original Bolívar Fuerte family entered into force on 1 January 2008. Printed by Giesecke+Devrient, De La Rue, and Oberthur Fiduciaire to the highest international security printing standards, these notes carry full intaglio printing, windowed security threads, denomination-specific portrait watermarks, and electrotype denomination watermarks.

Each denomination carries a distinct portrait of a significant Venezuelan historical figure — Guaicaipuro, Ezequiel Zamora, Francisco de Miranda, José Félix Ribas, Antonio José de Sucre, and Rafael Urdaneta respectively.

By 2015, inflationary pressure had rendered even the 100 Bs.F denomination inadequate for daily commerce, necessitating the denominational extension documented in Tier 2. Although they share the same premium print quality as Tier 2, these notes are not candidates for recirculation under the proposed ladder.

Their inclusion would create portrait redundancy — both tiers draw from the same gallery of Venezuelan historical figures, and circulating near-identical portraits across two denomination ranges would generate confusion at the point of transaction. The Tier 1 denominations are therefore retired in favour of the Tier 2 series, which maps cleanly to meaningful dollar equivalents at any plausible recirculation rate.

Tier 2 — Bolívar Fuerte (VEF / Bs.F) | G+D / De La Rue | Denominational Extension | 500 · 1,000 · 2,000 · 5,000 · 10,000 · 20,000 · 100,000

The formal ampliación ("denominational extension") of the Bolívar Fuerte family was announced on 4 December 2016 and confirmed by BCV press note on 16 January 2017.

The first shipment — 30 million pieces of the 1,000 Bs.F note — arrived from G+D in Sweden on 22 February 2017. These notes carry the same premium security specification as Tier 1: windowed security thread with demetallised BCV text, full intaglio printing, and denomination-specific portrait watermarks across the 500 through 20,000 Bs.F denominations.

No note in this series identifies itself as a "Bolívar Fuerte." Every note reads simply "BOLÍVARES" — the same word used across every subsequent monetary series.

One internal distinction within Tier 2 requires noting: the 100,000 Bs.F note breaks the denomination-specific portrait watermark continuity of the 500–20,000 series — carrying the version 2 Bolívar portrait watermark instead — and a numeral/text discrepancy on its face renders it irresolvably ambiguous under any legal tender declaration. The full watermark architecture is documented in Section 2.7. The 100,000 Bs.F is excluded from the proposed recirculation ladder on these grounds.

The 500 through 20,000 Bs.F denominations — confirmed vault stock of approximately 543 million notes — are the primary candidates for recirculation and constitute the core of the thesis's inventory argument.

Tier 3 — Bolívar Soberano (VES / Bs.S) | G+D / De La Rue | Original Family | 2 · 5 · 10 · 20 · 50 · 100 · 200 · 500

The original Bolívar Soberano family — printed in the United Kingdom by Giesecke+Devrient and De La Rue — entered into force on 20 August 2018 at 100,000:1 from the Bolívar Fuerte. These notes carry the same premium security specification as Tiers 1 and 2: full intaglio printing, windowed security threads, and watermark portraits. Each denomination carries a distinct portrait of a Venezuelan historical figure, consistent with the diverse gallery philosophy of the Tier 1 and Tier 2 series.

One watermark note: despite carrying diverse historical portraits on the obverse, the Tier 3 series uses the version 2 reincarnated Bolívar portrait as the watermark across all eight denominations. This was an operational decision driven by cost efficiency and the compressed 2018 reconversion timeline — commissioning eight individual denomination-specific watermark dies was not feasible within the available schedule, and the version 2 Bolívar die already existed from Tier 2 production. The watermark choice is a printing industry shortcut, not a design statement.

The Tier 3 notes — with confirmed unissued vault stock of approximately 210 million notes across the 2 through 200 Bs.S denominations — constitute the small-change layer of the proposed recirculation ladder. The 500 Bs.S is excluded on four grounds detailed in Section 2.8.

Tier 4a — Bolívar Soberano (VES / Bs.S) | Goznak | First Denominational Extension | 10,000 · 20,000 · 50,000

The first denominational extension of the Bolívar Soberano — Bs.S 10,000, 20,000, and 50,000 — bears a date of 22 January 2019 and entered circulation on 13 June 2019 as the first Ampliación del Cono Monetario of the Soberano era. The printer was Goznak, the Russian state security printing company, engaged as an emergency replacement following the US sanctions-driven payment crisis documented in Section 1.2. Goznak, operating outside the dollar-denominated SWIFT system, was the only available alternative at the time.

These notes are of materially lower quality than Tiers 1, 2, and 3. A single portrait of Simón Bolívar — the version 2 reincarnated portrait created following Chávez's 2012 exhumation and forensic facial reconstruction — appears on every denomination. Security features are reduced relative to the Western-printed tiers. These notes are not suitable for recirculation and are specifically excluded from the proposed denomination ladder. The June 2026 updated OFAC framework explicitly excludes Russian-linked entities from authorised Venezuelan commercial activity, confirming that any future authorised print programme would revert to Western printers rather than Goznak.

Tier 4b — Bolívar Soberano (VES / Bs.S) | Printer Unidentified | Second Denominational Extension | 200,000 · 500,000 · 1,000,000

The second denominational extension of the Bolívar Soberano — Bs.S 200,000, 500,000, and 1,000,000 — entered circulation from 8 March 2021. The printer of these notes has not been publicly identified. Analytically significant is that the typography of the numerical denomination value on these notes breaks with the Tier 4a Goznak series and matches the typography subsequently adopted in the Bolívar Digital series — indicating either a different printer from Goznak or a deliberate design continuity decision bridging the two monetary families. This remains unconfirmed from public sources.

These notes co-existed with the Bolívar Digital expression notes after 1 October 2021 under BCV Resolution 21-08-01, retaining legal tender status "until the BCV decides otherwise." The 1,000,000 Bs.S — the bridge instrument between the Soberano and Digital eras — was never formally demonetised; the BCV allowed managed devaluation to accomplish natural decirculation without a decree. These notes are not suitable for recirculation and are excluded from the proposed denomination ladder.

Tier 5 — Bolívar Digital (VED / Bs.D) | Printer Unidentified | Original Family | 5 · 10 · 20 · 50 · 100

The Bolívar Digital family entered into force on 1 October 2021 under the Nueva Expresión Monetaria, removing six zeros at 1,000,000:1 from the Bolívar Soberano. The printer has not been publicly identified; the typographic continuity with Tier 4b suggests a common or related printing source.

These notes carry the version 2 reincarnated Bolívar portrait across all denominations. Quality and security feature depth are assessed as comparable to Tier 4 — lower than the Western-printed tiers. These notes are not suitable for recirculation and are excluded from the proposed denomination ladder. They constitute the current circulating note family in Venezuela as of June 2026.

Tier 6 — Bolívar Digital (VED / Bs.D) | Printer Unidentified | Denominational Extension | 200 · 500

The denominational extension of the Bolívar Digital family added the 200 and 500 Bs.D notes. The printer remains unidentified. These notes are not suitable for recirculation and are excluded from the proposed denomination ladder. They represent the highest face value notes currently in circulation in Venezuela and will become the highest denominations in the existing circulating family if and when a recirculation of the legacy vault stock is announced.

Recirculation suitability summary:

| Tier | Series | Printer | Recirculation |

|---|---|---|---|

| 1 | Bolívar Fuerte original family | G+D / De La Rue / Oberthur | ✗ Portrait redundancy with Tier 2 |

| 2 | Bolívar Fuerte denominational extension | G+D / De La Rue | ✓ Primary candidates |

| 3 | Bolívar Soberano original family | G+D / De La Rue | ✓ Small-change layer |

| 4a | Bolívar Soberano first denominational extension | Goznak | ✗ Quality insufficient |

| 4b | Bolívar Soberano second denominational extension | Unidentified | ✗ Quality insufficient |

| 5 | Bolívar Digital original family | Unidentified | ✗ Quality insufficient |

| 6 | Bolívar Digital denominational extension | Unidentified | ✗ Quality insufficient |

2.2 The December 2015 Print Order — A Forward Programme

The Infosecura industry publication confirms that in late 2015 the BCV placed tenders for approximately 10.2 billion banknotes — structured as tranches of 2.6 billion, then 3 billion, totalling approximately 10 billion. This order is now understood to have covered both the Fuerte high denomination series and the 2018 Soberano UK-printed series simultaneously — a comprehensive forward programme for Venezuela's entire planned monetary transition, placed in a single tender.

The arithmetic supports this reading: the Fuerte high denomination series produced approximately 4.6 billion notes; the Soberano 2018 UK-printed series produced 4.89 billion notes; combined approximately 9.5 billion — consistent with the 10.2 billion tender, with the shortfall explained by the printers only bidding 3.3 billion due to payment concerns.

The trigger for this forward planning was June 2015 — when De La Rue first experienced payment delays due to US sanctions blocking SWIFT transactions. The BCV, recognising that its monetary supply chain was vulnerable to external political interference, responded by placing a comprehensive forward order covering not just the immediate denominations needed but the entire transition architecture planned for the following three years.

This is not crisis management. It is strategic institutional planning under extreme external pressure.

2.3 The BCV Official Circulation Data — Correcting the Vault Retention Claim

The author holds archived versions of the BCV's official circulation statistics file (9_3_2.xls — "Billetes en Circulación al Cierre de Cada Mes") downloaded from the BCV statistics page at multiple points between 2018 and 2026.

These files, combined with the companion flow file (9_3_4.xls — "Billetes Nuevos Puestos en Circulación"), provide the primary source data for the vault retention calculation.

The Cross-Check Confirmation

The two BCV files cross-check to within rounding error on every denomination — the cumulative flow totals in 9_3_4 match the peak stock figures in 9_3_2 to within 0.2 million pieces across all denominations. The BCV data is internally consistent and reliable.

The Vault Retention Calculation — Using May 2019 Freeze Values

A critical finding from the archived data: the BCV continued issuing Fuerte notes from April 2018 through August 2018 — four additional months of issuance after the Soberano launched. The final frozen values at May 2019 (when the Fuerte columns froze in the BCV data as the Soberano took over) are substantially higher than the April 2018 peak figures.

Using the May 2019 frozen values as the definitive circulation figure:

| Denomination | Max printed | Final circulation (May 2019) | Vault stock | Vault % |

|---|---|---|---|---|

| Bs.F 500 | 1,700M | 1,529.4M | 170.6M | 10.0% |

| Bs.F 1,000 | 1,500M | 1,421.2M | 78.8M | 5.3% |

| Bs.F 2,000 | 300M | 296.8M | 3.2M | 1.1% |

| Bs.F 5,000 | 600M | 400.9M | 199.1M | 33.2% |

| Bs.F 10,000 | 300M | 233.9M | 66.1M | 22.0% |

| Bs.F 20,000 | 400M | 374.4M | 25.6M | 6.4% |

| TOTAL | 4,800M | 4,520.2M | 543.4M | 11.3% |

Suggested Fuerte vault stock: approximately 543 million unissued notes — approximately $38 million in sunk production costs.

The 10,000 Bs.F is the strongest individual denomination argument: 22% vault retention, 66 million notes confirmed unissued by the BCV's own data, mapping to $100 at the optimal rate. The 5,000 Bs.F has 33% retention — 199 million notes, mapping to $50.

For the 2018 Soberano UK-printed series, the August 2024 BCV data shows the recirculable denominations (Bs.S 2 through 200) frozen at approximately 3,944 million notes in circulation against a total print run of approximately 4,154 million — leaving approximately 210 million notes confirmed unissued in vaults at a sunk cost of approximately $15 million.

Total suggested unissued vault stock: approximately 753 million notes, approximately $53 million in sunk production costs — verified by the BCV's own published data.

Why the Denominational Pattern Makes Sense

The pattern of vault retention is analytically informative. The 500 and 1,000 Bs.F notes — announced 16 January 2017 and desperately needed for daily commerce — were almost entirely distributed. The BCV had to keep releasing higher denominations as the dolartoday.com parallel rate unilaterally kept hyper devaluing. The 10,000 and 20,000 Bs.F notes were available from July and September 2017 respectively — but the devaluation was already so advanced that these denominations had limited useful life before becoming too small for daily commerce. The BCV metered their release and retained what the market had not absorbed.

2.4 The BCV Repatriation Hypothesis — An Additional Inventory Component

The vault stock of 543 million confirmed unissued Fuerte notes is the floor of the inventory available for recirculation. The hypothesis, supported by the market structure analysis in Section III, is that the BCV also recovered a meaningful quantity of circulated Fuerte notes from the foreign exchange market at La Parada, Villa del Rosario during the Phase 2 period (2017 to late May 2019).

The physical condition of repatriated notes: A Fuerte note that passed through the La Parada foreign exchange market followed a specific pathway that preserved its physical condition. Inside Venezuela, the note was treated as a financial instrument — recognised as carrying a significant premium over electronic Bolívar balances, it was passed from bank recipient to border-bound carrier without retail commerce use. At La Parada, the note was handled by FX dealers in a structured exchange operation — not in retail commerce where physical degradation occurs.

It could only have been purchased by BCV agents and transported back to Venezuela within approximately five to seven days of leaving the vault. Total time outside institutional custody: one week. Total use in retail commerce: zero.

G+D and De La Rue notes are engineered for two to three years of intensive retail circulation — tens of thousands of handovers, exposure to humidity, oils, and mechanical stress. A note that went through five to seven handovers over one week in a structured financial market and then sat in controlled storage for six years is physically indistinguishable from new.

The economics of repatriation: The BCV faced no currency risk on Bolívar holdings — it is the issuer. It could purchase notes at the prevailing parallel rate for a fraction of their production cost. By August 2018, 100,000 units of the 20,000 Bs.F notes that cost $7,000.00 to print could be purchased at approximately $400 — a 94.3% discount on the physical asset. By mid-October 2018, the same 100,000 units could be purchased at approximately $173 — a 97.5% discount. In barely two months, the discount on the physical asset widened by more than three percentage points, the parallel rate depreciating faster than the BCV could distribute. The BCV effectively acquired premium quality monetary instruments at steep discount.

The repatriation hypothesis addresses the central analytical anomaly in the La Parada market structure: a structurally one-sided market that cleared continuously, at scale, without trader inventory accumulation. The competing demand sources — and the volume, denomination-profile, and timing grounds on which each is excluded — are weighed in Section 3.1. The buyer that remains is the only candidate with both the motive and the balance sheet: the BCV.

The volume of repatriated notes cannot be quantified from public data. It represents an upside to the 543 million confirmed figure.

2.5 The Scalability Argument

The confirmed unissued stock is sufficient for an initial functional recirculation. Canada — the benchmark used throughout this section — circulates approximately 3 billion notes (roughly US$2,200 of cash per person) for a population of 40 million; Venezuela's population is approximately 28 million. 753 million notes across 13 denominations is operationally sufficient for a launch with a managed ramp-up.

Beyond the initial launch, the BCV can — with OFAC General License 57 in effect — contract with De La Rue, G+D, and Oberthur Fiduciaire for supplementary print orders. Crucially, any such order does not require designing new notes from scratch. The engraving dies, portrait artwork, security feature specifications, paper specifications, and printing plates for the existing Fuerte and 2018 Soberano series already exist at the printing facilities. Reordering from existing specifications is a fraction of the lead time and cost of commissioning a new note design.

However, supplementary print orders would require accessing hard currency currently supervised through the US Treasury deposit fund structure. The recirculation of existing vault stock requires no such payment — the notes are already paid for, the mechanism requires only a BCV Board resolution, and the execution requires only physical distribution logistics within Venezuela.

The scalability argument has a converse that supplies the strongest practical motivation for recirculation, and it can now be stated exactly, from the BCV's own files. At the end of June 2026 the entire circulating note stock of Venezuela — per the BCV's current 9_3_2 series (Cono Monetario Bolívar) — was 1,852.5 million pieces with a total face value of 86.08 billion Bolívars: 85.68 billion in the seven Bolívar Digital denominations plus 0.40 billion in the two frozen Soberano holdovers (Section 2.6).

At the 30 June official rate of 633.364 that is approximately US$136 million of physical cash for a country of roughly 28 million people — US$4.85 per capita, against the Canadian benchmark above: a gap of roughly 450-fold. It amounts to about 66 notes per person with an average value near seven US cents, and the highest-denomination banknote in the country — the 500 Bolívar note — was worth $0.79 at the end of June and under $0.70 by 10 July. Nor is this for want of effort: the BCV's own flow series (9_3_4) shows 376 million new pieces put into circulation in the first half of 2026 alone, expanding the note stock by 20% in pieces and 58% in face value in five months, with issuance of the 5 and 10 discontinued entirely and distribution concentrated in the 50 and 100.

The distribution machinery is demonstrably running; what it lacks is denominations — every note the BCV can currently distribute is worth less than one US dollar and shrinking daily. The recirculation is therefore not merely the cheap and fast option for rebuilding a domestic cash layer — against an 18-month minimum lead time for any new-family alternative, it is the only option available inside the window that matters.

2.6 The BCV Data Progression — Institutional Memory Management

The most analytically revealing finding from the author's multi-year archive of BCV statistical files is not the circulation numbers — it is the titles and scope of the files at each point in time. A newly incorporated, larger archive spanning September 2009 to August 2025 reveals that the BCV's nomenclature has not followed a single linear path toward erasure. It has oscillated — the Fuerte was demoted, then explicitly restored to co-equal status, then dropped again — a pattern of repeated active institutional decisions rather than passive drift toward a single outcome.

September 2009: "BILLETES EN CIRCULACIÓN AL CIERRE DE CADA MES" — no family qualifier at all. The earliest archived file, predating any of the family-naming conventions that follow.

May 2018: "...(FAMILIA ACTUAL)" — Single family: Bolívar Fuerte only. Called the "current family," published just before the Soberano launch.

May 2019: "...(CONO ANTERIOR Y FAMILIA SOBERANA)" — At the exact moment of the Soberano takeover, the BCV's internal statistical nomenclature explicitly demoted the Fuerte to cono anterior ("previous cone") — language that signals retirement, not mere supersession.

November 2020 – June 2022: "...(CONO BOLÍVAR FUERTE Y BOLÍVAR)" — The demotion was reversed. The Fuerte was restored to co-equal naming alongside the Soberano and Digital families, confirmed present across at least twenty months of archived snapshots. The BCV acknowledged the full picture for nearly two years after having explicitly retired the Fuerte in its own internal language the year before.

December 2022 – January 2025: "...(CONO BOLÍVAR Y NUEVA EXPRESIÓN MONETARIA)" — The Fuerte was dropped from the title and the data table entirely. This transition is confirmed by archive as already in effect by 23 December 2022 — approximately two months before Calixto Ortega departed the BCV presidency in February 2023. The decision to drop the Fuerte from published statistics was made under Ortega's own outgoing administration, not imposed by a successor.

August 2025: "...(CONO MONETARIO BOLÍVAR)" — The "Nueva Expresión Monetaria" reference was itself dropped. The title became a generic, era-neutral "Cono Monetario Bolívar" — no historical reference of any kind. This step predates the "January 2026 data only" finding below by approximately five months, showing that the simplification process continued incrementally rather than occurring in a single step at the moment of political transition.

June 2026 (current live file): Data starts from January 2026 only. All pre-2026 monetary history omitted from the published record.

This oscillating, seven-stage progression is not routine statistical housekeeping. The reversal at November 2020 is the critical data point: an institution executing a single-direction policy of erasure does not restore a demoted item to co-equal status for twenty months and then drop it again. What the record shows instead is a series of distinct institutional decisions, made at different points for what were likely different reasons, converging on the same eventual destination.

By January 2026 the BCV's published statistics contain no Fuerte series, no Soberano 2018 circulation history, no Goznak emergency series, no ampliación — a clean slate beginning at the moment of political transition, but arrived at through a longer and more deliberate process than a simple deletion narrative would suggest.

The June 2022 file — showing all three monetary families simultaneously — no longer exists on the BCV website. It exists only in the author's archive. The research compiled in this memorandum therefore holds documentary evidence of a statistical record that the BCV has progressively, and repeatedly, revised in its own published files.

The BCV's data management behaviour is itself evidence of the thesis. An institution that intended to permanently retire its legacy note inventory would have no reason to manage the data this carefully, or to restore a demoted series to prominence for nearly two years before dropping it again. The oscillation is consistent with — and only makes sense in the context of — preserving the optionality that the recirculation thesis describes.

The primary files, read directly (July 2026). The author holds thirty-five archived snapshots of the BCV's 9_3_1, 9_3_2, and 9_3_4 series spanning September 2009 to June 2026, now permanently archived (see bibliography). Read directly, they add four facts to the progression above. First, the 547.875634 million freeze is identified: it is the combined stock of the only two denominations

Resolution 24-08-01 never touched — 299.986329 million pieces of the 500,000 and 247.889305 million of the 1,000,000 Bs.S — frozen since the third quarter of 2022 and still carried, line by line, on the BCV's current 2026 circulation table.

Second, the December 2022 snapshot contains a literal "R E C O N V E R S I Ó N" marker row at October 2021, with the Soberano piece-counts running through it unchanged: the BCV's own ledger treats the re-expression as a non-event for the physical stock — the nominal continuity doctrine of Section 1.8, documented from inside the Bank's own statistics.

Third, the treatment of legacy stock follows a repeated three-step pattern — freeze, carry, drop. The Fuerte circulation columns froze at 10,100.4 million pieces in December 2019, were carried unchanged for three full years, and were dropped in the December 2022 retitle; the Soberano columns froze through 2022, were carried, and were dropped — all but the two Resolution 24-08-01 survivors — at the August 2025 retitle. Nothing is ever written off: it is frozen, carried, and then removed from view.

Fourth, a refinement to the seventh stage: the August 2025 "Cono Monetario Bolívar" file is already current-year-only, so the omission of history dates to the 2025 format change, and the January 2026 baseline is that format's routine year-roll rather than an independent act.

A structural note: the data management progression documented above spans four BCV presidencies. The December 2022 dropping of the Fuerte occurred under Ortega's outgoing administration; the stabilisation-era files were maintained under Pérez Abad (February 2023–April 2025); the August 2025 "Cono Monetario Bolívar" simplification occurred under Guerra Angulo (April 2025–April 2026); and the January 2026-baseline file is now maintained under Luis Pérez, appointed April 2026. Whether the current BCV Board under President Pérez is oriented toward the recirculation mechanism embedded in this architecture is a question this research cannot answer from public data.

2.7 Portrait Continuity and the Denomination-Neutral Design

No note in any Venezuelan monetary series from 2008 to 2024 identifies itself by series name. No note says "Fuerte." No note says "Soberano." Every note across every series reads "BOLÍVARES" — the same word, the same issuing authority, the same physical dimensions of 156 × 69 mm. The portrait architecture reflects the continuity philosophy:

Fuerte series and 2018 Soberano UK-printed: Diverse gallery — one significant Venezuelan historical figure per denomination (Guaicaipuro, Zamora, Miranda, Ribas, Sucre, Urdaneta, Rodríguez, Bolívar). The finest physical monetary instruments Venezuela has produced.

2019 Goznak series and subsequent Digital: Single repeated portrait of Simón Bolívar — the version 2 reincarnated portrait created following Chávez's 2012 exhumation and forensic facial reconstruction of Bolívar's remains. Lower quality engraving throughout.

2.8 The Proposed Denomination Ladder

The recirculation thesis proposes thirteen denominations combining the surviving 2018 Soberano lower denominations with the Fuerte high denomination vault stock:

| Denomination | Series | USD equivalent at 100 Bolívars per dollar |

|---|---|---|

| 2 Bs | Soberano 2018 | $0.02 (may not be actively distributed) |

| 5 Bs | Soberano 2018 | $0.05 — Canadian model minimum floor |

| 10 Bs | Soberano 2018 | $0.10 |

| 20 Bs | Soberano 2018 | $0.20 |

| 50 Bs | Soberano 2018 | $0.50 |

| 100 Bs | Soberano 2018 | $1.00 |

| 200 Bs | Soberano 2018 | $2.00 |

| 500 Bs | Fuerte 2017 | $5.00 — WORKHORSE |

| 1,000 Bs | Fuerte 2017 | $10.00 — WORKHORSE |

| 2,000 Bs | Fuerte 2017 | $20.00 |

| 5,000 Bs | Fuerte 2017 | $50.00 |

| 10,000 Bs | Fuerte 2017 | $100.00 |

| 20,000 Bs | Fuerte 2017 | $200.00 |

Excluded: 500 Bs.S — four grounds: (a) portrait redundancy — carries the version 2 reincarnated Bolívar portrait that defines the Goznak/Digital era, creating visual confusion in the ladder; (b) replaced by the superior 500 Bs.F which maps to the same $5.00 value with a diverse historical portrait; (c) would introduce the "wrong" Bolívar portrait into the premium-quality denomination ladder; (d) visual clarity for domestic users and tourists — no note with the version 2 reincarnated Bolívar should be in the recirculated series, so that the portrait stands as a clear visual identifier of the pre-recirculation era.

Excluded: 100,000 Bs.F — three grounds: (a) redundant to the 20,000 Bs.F; (b) numeral/text discrepancy — the note displays "100" but written text reads "CIEN MIL BOLÍVARES," creating irresolvable ambiguity under any legal tender declaration at face value in Bolívars decree; (c) the original three-zero reconversion plan would have mapped it to 100 Bs.S, which would have made co-circulation easier as people would have seen 100 Bs.F and 100 Bs.S and been less reluctant to exchange the old notes for the new.

2.9 The Face-Value Injection — Monetary Base Impact

The vault stock has appeared in this memorandum so far as an asset — approximately $53 million in sunk production cost. A recirculation declaration converts it into a liability, and the memorandum must run that arithmetic itself rather than leave it to a hostile reviewer.

The vault stock injection. At face value in Bolívars under the nominal continuity doctrine, the confirmed Fuerte vault stock from the Section 2.3 table totals:

| Denomination | Vault stock (notes) | Face value (Bolívars) |

|---|---|---|

| Bs.F 500 | 170.6M | 85.3B |

| Bs.F 1,000 | 78.8M | 78.8B |

| Bs.F 2,000 | 3.2M | 6.4B |

| Bs.F 5,000 | 199.1M | 995.5B |

| Bs.F 10,000 | 66.1M | 661.0B |

| Bs.F 20,000 | 25.6M | 512.0B |

| Total | 543.4M | ≈2,339B (2.34 trillion) |

At a Stage 1 rate of 700 Bolívars per dollar, full distribution of the vault stock injects approximately $3.3 billion of physical base money; at the 100 Bolívars per dollar target, the same notes represent approximately $23.4 billion.

The Soberano vault stock (210 million notes, all denominations of 200 Bolívars or below) is bounded above by 42 billion Bolívars — immaterial by comparison — and the circulating Soberano small-change layer (approximately 3.94 billion notes of 200 Bolívars or below) is bounded above by roughly 790 billion Bolívars, with the true figure far lower given the denomination mix.

The publicly held contingent liability. If the recirculation declaration extends to publicly held Fuerte notes — as the wealth-distribution argument of Section 3.3 assumes — the ceiling is far larger. At the April 2019 circulation peak recorded in the BCV's own 9_3_2 series, 4,256.6 million notes of the six Tier 2 denominations were in public circulation, carrying a total face value of approximately 14.6 trillion Bolívars. The ledger ceiling of the liability is no longer speculative. Through the 2019 deposit window the BCV's circulating count for these denominations fell to 2,925.9 million pieces and then froze — carried unchanged on the Bank's own files from December 2019 until the Fuerte columns were dropped in December 2022 (Section 2.6). By the BCV's own accounting, 68.7% of Tier 2 pieces — 9.65 trillion Bolívars of face value — were never presented (approximately $13.4 billion at the 10 July rate; $96.5 billion at the 100 target).

The ledger figure is a ceiling, not an estimate of physically surviving notes — never-presented includes destroyed and lost, and destruction was concentrated in the lower denominations (Section 3.2), while the high denominations were issued late, circulated briefly, and were hoarded in bricks precisely because of the cash premium documented in Section 3.1. The physical overlay therefore remains a scenario, bounded above by the ledger:

| Public survival rate | Surviving face value | USD at 700/$ | USD at 100/$ |

|---|---|---|---|

| 5% | ≈0.73 trillion | ≈$1.0B | ≈$7.3B |

| 15% | ≈2.19 trillion | ≈$3.1B | ≈$21.9B |

| 30% | ≈4.38 trillion | ≈$6.3B | ≈$43.8B |

The tension this creates — stated honestly. The Stage 3 appreciation mechanism (Section 5.5) requires the BCV to sell dollars and buy Bolívars, contracting Bolívar supply — while the recirculation simultaneously expands the physical note supply by a large multiple of the existing stock: the vault inventory's 2.34 trillion at face is 27 times the entire circulating note stock recorded in the BCV's 30 June 2026 file (86.08 billion Bolívars — Section 2.5), and the Tier 2 ledger-outstanding is 112 times it. (Bolívar sight deposits are a separate and larger aggregate; the multiple stated here is physical cash against physical cash.)

The injection and the appreciation compete for the same reserve ammunition. Four considerations govern whether this tension is manageable rather than fatal. First, the injection is fully controllable in tempo: the BCV demonstrated in 2017 that it meters distribution deliberately (Section 2.3), and vault stock enters circulation only as the BCV releases it — the declaration creates the legal status, not the physical flow.

Second, the publicly held component is a design variable, not an obligation: the Board can recirculate vault stock alone (Section 1.6), capping the Stage 1 injection near $3 billion, and defer or condition the re-monetisation of public holdings.

Third, the demand side is not static: a credibly appreciating Bolívar in a cash-starved, informally dollarised economy is precisely the environment in which Bolívar cash demand can expand to absorb new supply — the 2003 BVC episode documented in Section 5.6 is the historical demonstration that Bolívar-denominated instruments attract massive demand when they become the credible available store of value.

Fourth, on the government's own framing the injection is partly the point: Section 3.3's wealth distribution is a deliberate recapitalisation of household balance sheets, funded by seigniorage on notes that cost $53 million to produce.

The memorandum's position is therefore not that the injection is small — it is not — but that it is meterable, partitionable, and partially self-absorbing, and that any credible recirculation design would sequence it against reserve capacity. What the thesis cannot survive is a version of the recirculation that declares everything at once and appreciates simultaneously; no such version is proposed here.

SECTION III: MARKET EVIDENCE — WHAT THE SECONDARY MARKET REVEALS

The physical vault inventory documented in Section II does not exist in isolation. A secondary market for Venezuelan banknotes has operated continuously since 2014, providing real-world pricing, circulation data, and behavioural evidence that independently corroborates the central claims of the thesis.

Unresolved observation: Uncirculated sequentially numbered Fuerte bricks have been observed at La Parada carrying Banco do Brasil packaging labels — consistent with inventory staged for a Brazilian secondary distribution channel (through Roraima state — Pacaraima and Boa Vista) that operated during approximately 2016 to mid-2017 before closing, with the flow rerouting to La Parada. This observation is factually confirmed through direct field observation; the explanation remains an inference.

3.1 The La Parada, Villa del Rosario Physical Currency Market — Three Phases

The border community of La Parada within Villa del Rosario — directly at the Simón Bolívar International Bridge crossing point — hosted a physical Bolívar currency market from approximately 2014 through early 2020.

A critical clarification on market geography: the physical cash Bolívar market operated at La Parada, not in Cúcuta city itself. Cúcuta is the broader metropolitan area several kilometres into Colombia. Cúcuta merchants had long since stopped accepting Bolívars for any retail transactions.

La Parada was exclusively a foreign exchange operation. Venezuelan territory on the other side of the bridge — San Antonio del Táchira — did not participate in Bolívar trading due to legal restrictions on currency dealing inside Venezuela.

The reference rate published by DolarToday during the La Parada market's active period (2010–2019) is documented in the operator's own words and in a US federal complaint as being derived from calls to Colombian border dealers.

Defendant Altuve — one of DolarToday's principals, operating from Doral, Florida — described the methodology in a 2015 interview: calls to "several currency traders in Cúcuta, a Colombian border city," converting the Bolívar-to-peso exchange rate into dollars, with the caller concealing his identity to avoid influencing quotes. The BCV's own complaint in Banco Central de Venezuela v. DolarToday LLC et al. (D. Del., Case No. 1:15-cv-00965, filed 23 October 2015) accepts the same framing but alleges the published rate was "magnitudes" above the actual rates charged by border exchange houses.

The thesis's field research provides finer geographic resolution than either account: the Colombian border FX market referenced as "Cúcuta" by DolarToday comprised dealers operating across La Parada at the bridge crossing, the Parque Santander cluster in Cúcuta city, and the Alexandria market — with many established dealers maintaining operations in more than one location simultaneously. The "Cúcuta" label in both Altuve's account and the BCV complaint is shorthand for this entire cross-border dealer ecosystem, not a precise geographic designation. The thesis's naming of specific market locations within that ecosystem is additive to the existing record, not corrective of it.

The Cash/Electronic Premium — The Core Market Dynamic

A fundamental feature of the Venezuelan monetary situation during 2017-2019 that shaped the entire La Parada market was the price differential between physical cash Bolívars and electronic Bolívar balances:

Inside Venezuela: Physical cash commanded approximately a three-times discount over electronic payment for the same transaction. A bus ticket in Caracas in July 2018 cost 1,000,000 VEF in physical cash but 3,000,000 VEF by debit card at the same kiosk. Physical cash was scarce, useful in Venezuela's predominantly informal cash economy, and priced accordingly.

At La Parada: An FX dealer in July 2018 would sell electronic Bolívars (bank transfer to a Venezuelan account) at the parallel rate of approximately 5,000,000 VEF per USD. Physical cash Bolívars cost approximately three times more in dollar terms — at approximately 1,600,000 VEF per USD. Physical notes were scarcer and more valuable in dollar terms because they could function in Venezuela's cash economy where electronic balances often could not.

The arbitrage was therefore not simply between the official rate and the parallel rate. It was between two parallel rates for the same currency — one for physical notes and one for electronic balances — driven by the structural scarcity of cash inside Venezuela and the premium it commanded in daily commerce.

Phase 1 — Emergence and Arbitrage (2014–2017)

Before the La Parada physical cash market emerged as the dominant parallel FX mechanism, Venezuelan parallel rate discovery passed through two prior structural phases that are directly relevant to the dataset analysed in Section IV.

From 2003 to May 2007 — the period following the implementation of exchange controls — the dominant parallel rate mechanism was the CANTV ADR arbitrage: investors purchased CANTV shares in Bolívars on the Bolsa de Valores de Caracas and sold the corresponding NYSE ADR in dollars, with the implied exchange rate constituting the de facto parallel rate.

Garay & González (2012), in an empirical study of Venezuelan ADRs published in INNOVAR, document this mechanism in detail: following the February 2003 exchange controls, CANTV local share prices rose 261% while NYSE ADR prices rose only 50.32%, and trading volumes in local CANTV shares increased 443.6% — all driven by investors using the legal ADR conversion channel as a capital escape valve. Garay & González characterise the ADR discount that emerged — reaching 50% in January 2004 — as "the market's prediction concerning the expected future devaluation in the official exchange rate," a forward-pricing function structurally identical to what the Yadio parallel market performs today.

CANTV was nationalised in May 2007, ending this specific arbitrage channel. The period from May 2007 to January 2010 — between the CANTV nationalisation and DolarToday's January 2010 launch — was dominated by the bond permuta mechanism and the "Lechuga Verde" rate aggregator, with the rate derived from transactions in Bolívar-denominated bonds exchanged for dollar-denominated sovereign instruments through local brokerage houses, until the CNV shut down these operations in June 2010.

The La Parada Bolívar market originated in the gap between official and parallel rates, attracting three categories of participants:

Venezuelan economic refugees: The primary flow — people fleeing economic collapse carrying remaining Bolívar assets as their last portable store of value.

Commercial merchants: Structured traders travelling to La Parada to exchange Bolívars for Colombian pesos, then purchasing goods for import back into Venezuela.

General capital flight: Opportunistic arbitrageurs (active from 2014–2015); business owners and individuals liquidating Bolívar holdings (mid 2016–December 2017); anyone moving remaining small values out of Venezuela through the most accessible means available.

All Fuerte denominations flowed to La Parada. There was no preference between denominations — what reached La Parada was whatever the Venezuelan banking system and commerce were releasing at any given moment. More 1,000 Bs.F notes reached La Parada in April 2017 because that was what the banking system was distributing; more 10,000 and 20,000 Bs.F notes from July and September 2017 as those denominations became available.

Phase 2 — Peak Activity and the BCV Repatriation Hypothesis (2017–late May 2019)

The corrected arbitrage pathway: A Fuerte note did not simply "circulate" in the conventional sense. Its journey was as follows:

- Step 1 — Bank issuance: The note leaves BCV vault, is distributed to a commercial bank, and received by a customer — typically a business or individual requesting higher denomination notes. Pristine condition.